You can defend your home from foreclosure. But, you need some specific information.

When lenders securitized mortgages then swapped and traded them as derivatives, they bundled notes and mortgages as “series” rather than physical bundles of paper documents. Most lenders didn’t keep track of the original notes ~ for instance, Mortgage Lenders Network USA, had 22,100 boxes of original loan papers in just one location, and, they didn’t want to pay for ongoing storage.

The original note is the evidence of the debt in a foreclosure. The UCC deals specifically with the original note in foreclosures.

“The UCC provides that there are three scenarios in which a person is entitled to enforce a negotiable instrument such as a promissory note: (1) when that person is the holder of the instrument; (2) when that person is a non-holder in possession of the instrument who has the rights of a holder; and (3) when that person does not possess the instrument but is still entitled to enforce it subject to the lost-instrument provisions of UCC Article 3. Section 55-3-301. To show a “direct and concrete” injury, Deutsche Bank needed to establish that it fell into one of these three statutory categories that would establish both its right to enforce Homeowner’s promissory note and its basis for claiming that it suffered a direct injury from Homeowner’s alleged default on the note.” Deutsche Bank v. Johnston, 369 P.3d 1046 (2016)

When the foreclosing party does not have the original note, endorsed to them or in blank, and attaches to the Complaint no evidence that they are the holder of the Note, they can still achieve standing if they can show that the Note was lost while it was in their possession… Failing that, they can have their “standing” to foreclose challenged.

Standing is the right to proceed as a party to the law suit. If a would-be plaintiff does not have standing, then in a Federal Court, the court has no jurisdiction to rule on the case. In a state court, like New Mexico, the Court has jurisdiction, but the would-be plaintiff can be precluded from foreclosing by lack of standing.

While it’s best to address standing in your answer to the foreclosure complaint, the issue of standing and jurisdiction can be raised at any point in a law suit.

In most cases the original note does not become an issue or deciding factor unless YOU raise it. If you are already in foreclosure, look at the mortgage and note attached to the complaint: Is the note endorsed to the plaintiff? If not, is there any evidence attached to show that the plaintiff is the holder? Do Discovery and ask your lender to produce the Original Note. That way you will have a clear answer showing that they do or do not have the original note.

Lost Note Affidavit

Of course, your lender will likely file a Lost Note Affidavit saying they had the note, but lost it. This, they hope, will allow them to sidestep the UCC requirement to produce the Original Note. That’s because the UCC allows for foreclosure if the lender had the note, but lost it.

In my case, I’m quite sure Wells Fargo never had the original note. I’m sure they wrote their Affidavit of Lost Note trusting that the lie would carry the day. And, in fact it kept me from winning the hearing on my motion to dismiss for lack of standing.

Having lost the hearing the mediation process began, which is required here in New Mexico prior to any foreclosure judgment.

I don’t trust Wells Fargo because: 1. They denied me due process when they filed the Foreclosure Complaint and didn’t serve me, and 2. They qualified me for a HAMP loan modification trial period, which I kept, then they reneged. So, if Wells Fargo should turn out to be as tricky in mediation as they were in earning my distrust, I want to be prepared for trial.

To get a handle on how to attack the Original Note copy, I called several forensic evidence people. The conversations I had led me to a forensic auditor who works with foreclosure defense lawyers. I won’t list his name and number, yet, because I don’t know how good he is. But, what I do know is that he suggested I do a Qualified Written Request for the things I was not able to get Wells Fargo to produce in Discovery, and to address certain questions relating to the Original Note.

My Qualified Written Request ~ Read more.

Original Note and Standing

Standing is the stake or interest, protected by law, that an individual or entity has in a dispute that entitles him to bring the controversy before the court for judicial relief. The doctrine of “standing” comes from the Constitution, Article 3. Read more.

The U.S. Supreme Court has made it clear that the burden of establishing standing rests on the plaintiff. From initial pleading through summary judgment and trial—the plaintiff must carry that burden. Of particular importance is the fact that, per the opinion of the U.S. Supreme Court, standing must exist on the date the complaint is filed and throughout the litigation. And, standing can be challenged at any time in the litigation, including on appeal, by the defendants or, in some circumstances, by the court sua sponte. Plaintiffs must demonstrate standing for each claim and each request for relief. There is no “supplemental” standing: standing to assert one claim does not create standing to assert claims arising from the same nucleus of operative facts.

Federal Practice Manual for Legal Aid Attorneys re Standing ~ Read more.

In a foreclosure, in order for the plaintiff to have standing, the plaintiff must be in possession of the Original Note with proper indorsements. This is because the UCC, Uniform Commercial Code, which each state in the United States has adopted in its statutes, requires that the original note be in the possession of the entity seeking foreclosure of the note.

If you are served with foreclosure papers the issue of the original note is one you must raise. That is to say, the plaintiff will be acting as if it has standing, whether that is actually true, or not. Immediately raising the issue, as a Defense, will either stop the foreclosure and cause it to be dismissed, or it will cause the court to rule that the plaintiff must provide the original note.

Answers, Defenses and Counterclaims ~ Read more.

Judicial Foreclosures

In a judicial foreclosure state a court case comes into being when the foreclosure is filed. You must respond to the Foreclosure Complaint within the specified time in order to retain your rights. In your Objection to the Complaint you must raise the issue of the Original Note and standing in order for you to get early benefit from the doctrine of standing and the plaintiff’s lack of the original note. You do this by stating the issue as a defense.

A copy of the note may be attached to the Complaint. A copy is not an original. A copy may have some indorsements shown, but it may not have the indorsement to the plaintiff in your foreclosure. Proper endorsements are an additional critical issue.

Excellent list of cases in which Original Note featured ~ Read more.

In a Non-Judicial Foreclosure State

In non-judicial foreclosures the mortgage contract provides for foreclosure without the lender filing in court. Therefore, if you want to stop the foreclosure using critical issues, you must file a court case. Read more.

My Motions re the Original Note

I didn’t know about the UCC’s requirement that the plaintiff be in possession of the original note until I found, on the internet, a long decision written by a judge in New York.

Because I’d never heard of the concept before I wondered whether it applied in my state. Sure enough, it did. So, I wrote the motion below, fully expecting the case to be dismissed. Silly me.

Although the case was not dismissed, the Court filed its own order saying that the plaintiff must produce the Original Note and deposit it with the court clerks to put in the vault, before the plaintiff could file a Motion for Summary Judgment. Thereafter the plaintiff did nothing much for just over two years.

You can see how much my understanding of the note progressed by comparing the two pleadings below, to my Defendant’s Motion for Summary Judgment, filed in 2015. See Defendant’s Motion for Summary Judgment.

FIRST JUDICIAL DISTRICT COURT

COUNTY OF SANTA FE

STATE OF NEW MEXICO

No. D-101-CV-200800942

Wells Fargo Bank NA,

…..Plaintiff,

Karen Marie Kline, Pueblos de Rodeo Road Owners

Association, Inc.; Manhattan Condominium Association,

…..Defendants.

MOTION TO ABATE OR DISMISS WITH PREJUDICE FORECLOSURE PROCEEDINGS

….COMES NOW Defendant, Karen Marie Kline, pro se (“Kline”) and hereby moves this honorable court to abate foreclosure proceedings.

- On April 7, 2008, the Plaintiff commenced foreclosure proceedings against the Defendant and the real property which is the subject matter of this litigation.

- On April 7, 2008, Summons was issued to Karen Kline.

- There was no service to Karen Kline and no Return of Service is filed.

- Plaintiff lacks standing to bring this action: Wells Fargo has presented no evidence that it, in any manner, possessed the subject mortgage and note on April 7, 2008.

- Plaintiff has shown by the mortgage and note attached to plaintiff’s Complaint that my mortgage and note were made with GE Capital. It therefore follows that GE Capital has standing to be plaintiff in a foreclosure of said note and mortgage insofar as the note and mortgage are nonnegotiable.

- Wells Fargo (“WF”) has failed to provide any evidence of my note and mortgage being sold or assigned by GE Capital to Wells Fargo and as a result it appears on its face that Wells Fargo does not have standing to foreclose my mortgage and note as a nonnegotiable instrument.

- If my note and mortgage were originally negotiable or were securitized with the resulting instrument being negotiable, it falls under the UCC definition of a negotiable instrument provided by New Mexico Statute 55-3-104:

“negotiable instrument” means an unconditional promise or order to pay a fixed amount of money, with or without interest or other charges described in the promise or order, if it:

(1) is payable to bearer or to order at the time it is issued or first comes into possession of a holder;

(2) is payable on demand or at a definite time; and

(3) does not state any other undertaking or instruction by the person promising or ordering payment to do any act in addition to the payment of money, but the promise or order may contain (i) an undertaking or power to give, maintain, or protect collateral to secure payment, (ii) an authorization or power to the holder to confess judgment or realize on or dispose of collateral, or (iii) a waiver of the benefit of any law intended for the advantage or protection of an obligor.

“Instrument” means a negotiable instrument.

- The note created by defendant Kline is clearly a negotiable instrument as that term is defined by the UCC, New Mexico Statute, Chapter 55, Article 3. In the terms of the statute, the note is payable to bearer or to order, and it is payable on demand or at a definite time.

- If the subject mortgage and note were securitized, securitization was done without notice to borrower.

- Under the provision of the UCC, NMSA 55-3-301, the person seeking to enforce the note must have possession.

- Separate questions presented are whether the note was in fact physically transferred to plaintiff, when that would have occurred and whether the note had been endorsed prior to that time. Those issues have to be addressed before one can determine whether the plaintiff was a person entitled to enforce the note pursuant to the UCC, New Mexico Statute Chapter 55, Article 3, at any particular time.

- Plaintiff’s complaint provided no information as to possession of the note.

- Plaintiff filed its motion for summary judgment based upon a copy of the note and mortgage and modification alone. Additional documentation beyond that was not provided.

- Although Wells Fargo Home Mortgage division of Wells Fargo Bank NA is a member of the MERS Servicer Identification system, Exhibit 1, page 1, my mortgage is not found in the system. I checked using each of the two possible zip codes. Exhibit 1, pages 2-3.

- In 2005, I tried in good faith to pay off my mortgage, as recounted in my Requests for Admissions to Wells Fargo. See Defendant’s Motion to Deem Admitted which is incorporated here by reference.

- In 2005, Wells Fargo, in bad faith, went back on its word to my listing agent for my single family rental that if I had a quick closing on my single family rental and as a result had the money to pay Wells Fargo that Wells Fargo would stop the foreclosure auction. See Defendant’s Motion to Deem Admitted.

- In 2005, Wells Fargo, also in bad faith, refused to accept my offer to pay off my mortgage from the proceeds of the closing on my single family rental. See Defendant’s Motion to Deem Admitted.

- Despite the above described irregularities and problems I, in good faith, requested to have my mortgage modified under the terms of the Emergency Economic Stabilization Act of 2008, 12 U.S.C §5201, §5219, for which I and my property qualify.

- U.S. Treasury guidelines for the Act are published under the title of Home Affordable Modification Program (“HAMP”).

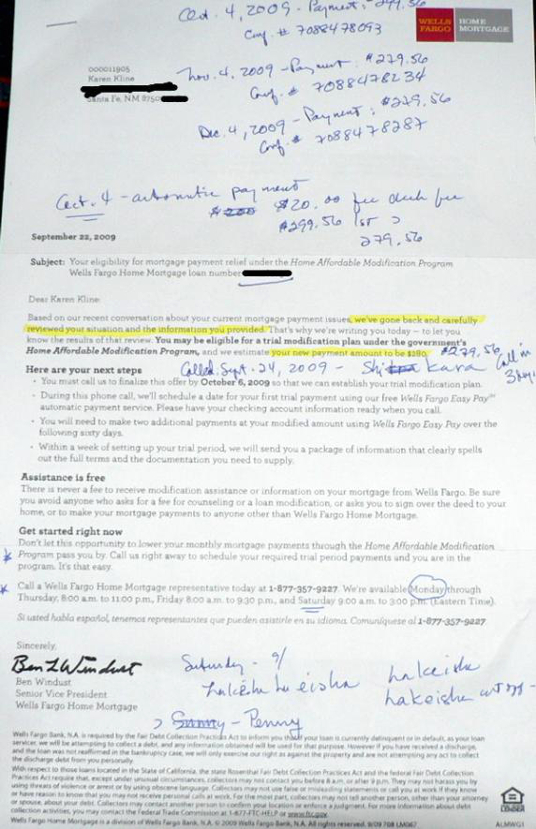

- On September 22, 2009, Wells Fargo responded positively to my repeated requests and sent me a letter offering me a HAMP trial period. Exhibit 2.

- Wells Fargo’s letter said I had to finalize the offer by October 6, 2009. Exhibit 2.

- I called to finalize and set up the three required trial period payments on September 26, 2009 and I noted my prearranged payments on the top of the letter, to include their confirmation numbers. Exhibit 2.

- My first confirmed payment was on October 4, 2009, which was before the finalization deadline. Exhibit 2.

- U.S. Treasury HAMP guidelines, page 3, require that foreclosures be stopped during the trial period.

- Wells Fargo refused to vacate its October 19, 2009 hearing on its Motion for Summary Judgment.

- The action was stayed by the Court’s order, entered October 26, 2009.

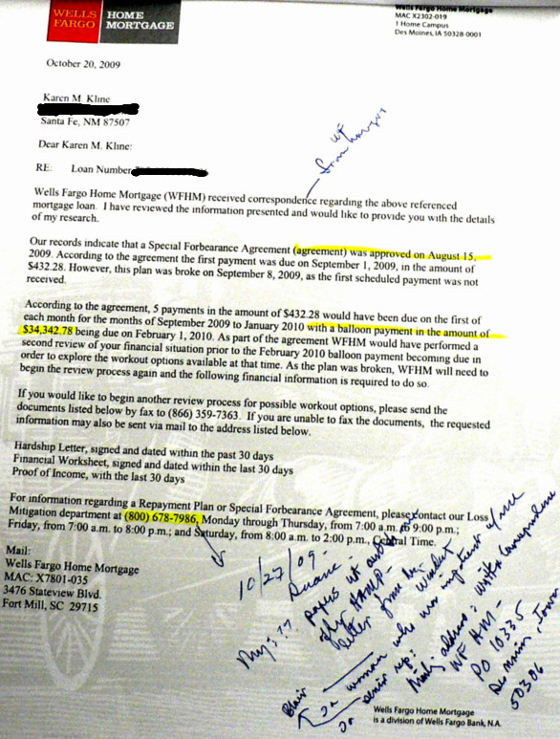

- On October 20, 2009, WF sent me a letter saying I had to start the review process again based on correspondence Wells Fargo had received. Exhibit 3.

- When I called Wells Fargo I was told the correspondence was received on October 20, 2009 and was from Wells Fargo’s lawyers. See my notes, Exhibit 3.

- All three of my trial period payment checks were cashed by Wells Fargo per their confirmation numbers. Exhibit 2.

- Wells Fargo never sent me the package of information it promised in its September 22, 2009 letter. Exhibit 2.

- Wells Fargo denied my loan modification in bad faith.

- When I complained to the Office of the Comptroller of Currency, which is the correct procedure, Wells Fargo’s bad faith answer was that the case was in active litigation, which Wells Fargo knew to be untrue given that the case had been stayed by the Court.

WHEREFORE for the above described reasons I respectfully request that this honorable Court dismiss this action with prejudice.

Respectfully submitted,

Karen Marie Kline

XXXXXXXXXX

Santa Fe, New Mexico 87507

(505) XXX-XXXX — email: Methylcobalamin1@msn.com

CERTIFICATE OF SERVICE: I caused a true copy of the above MOTION TO ABATE OR DISMISS WITH PREJUDICE FORECLOSURE PROCEEDINGS to be mailed today, September 23, 2010, to:

Castle, Meinhold and Stawiarski

Renae Richards Charney

20 First Plaza NW Suite 602

Albuquerque, NM 87102

I’m not showing the exhibits in the interest of saving space.

The Court deferred to Wells Fargo and did not abate or dismiss.

My Lost Note Brief

I didn’t know about the UCC’s requirement that the plaintiff be in possession of the original note until I found on the internet a long decision written by a judge in New York. At the hearing on July 25, 2011, I said the following:

Under the provisions of the UCC, NMSA 55-3-301, the person seeking to enforce the note must have the note in its possession. Wells Fargo did not have the original note and mortgage in its possession when it filed to foreclose. Further, Wells Fargo has not produced the original note and mortgage in response to my Requests for Production, for which Certificate of Service was filed more than two years ago on May 26, 2009. Without the original note in its possession Wells Fargo did not have the right to file for foreclosure of the negotiable instrument which my mortgage note was. To proceed deceptively as if it had the original note and mortgage shows unclean hands on the part of Wells Fargo and its lawyers.

I did not succeed on the theory of unclean hands. But, the judge ordered that the plaintiff and I file briefs re Lost Original Note. Below is a copy of my brief. The beginning focuses on why Wells Fargo Lost Note Affidavit was inadequate, the later part focuses on why Wells Fargo should not be allowed to foreclose given that it qualified me for loan modification, then reneged.

FIRST JUDICIAL DISTRICT COURT

COUNTY OF SANTA FE

STATE OF NEW MEXICO

Wells Fargo Bank NA,

Plaintiff, No. D-101-CV-200800942

v.

Karen Marie Kline,

Pueblos de Rodeo Road Owners Association, Inc.

Defendants.

DEFENDANT KAREN MARIE KLINE’S BRIEF ON LOST ORIGINAL NOTE

COMES NOW Defendant Karen Marie Kline and files a brief on lost original notes and foreclosure:

Plaintiff’s Affidavit of Lost Original Note shows by a copy of the note that it was not endorsed to Wells Fargo. The affidavit does not give the date the original note was shipped, the means by which it was shipped, the tracking information related to the shipping, nor any explanation of how the tracking information failed to locate the original note.

With these deficiencies Wells Fargo’s Affidavit of Lost Original Note fails to show that the loss of possession was not the result of transfer or lawful seizure, either of which would preclude Wells Fargo from foreclosing on the negotiable instrument pursuant to the UCC, 55-3-309(2) NMSA 1978. The Affidavit of Yolanda T. Williams may not be relied upon when it lacks evidence to support its statements.

Discussion

New Mexico’s UCC statute, 55-3-309(b) NMSA provides that:

A person seeking enforcement of an instrument under Subsection (a) must prove the terms of the instrument and the person’s right to enforce the instrument.

In this case, Wells Fargo must prove that the instrument was not lost in a transfer in order for Wells Fargo to prove its right to enforce the instrument pursuant to 55-3-309(a)(ii) NMSA.

There is no question but that I signed a Note and Mortgage on my home at 3255 Calle de Molina, Santa Fe, New Mexico. The question is whether Wells Fargo, The Bank of Texas, GE Capital Mortgage Services or any other lost the note as a result of a transfer of the note. No evidence has been presented by Wells Fargo to show that the loss of the Note was not a result of transfer.

Foreclosing under the terms of the Mortgage

First: The Order Governing Summary Judgment and Default Judgment Procedures in Foreclosure Actions, filed January 7, 2011, says Plaintiff must verify that it made a reasonable attempt to resolve the matter.

Plaintiff cannot so verify because Plaintiff sent Defendant a letter, Exhibit 1, saying, “we’ve gone back and carefully reviewed your situation and information… that’s why we’re writing you today…you may be eligible for a trial modification plan under the government’s Home Affordable Modification Program…You must call us to finalize the offer… During the phone call we’ll schedule a date for your first trial payment… You will need to make two additional payments at your modified amount…”

Defendant complied but Plaintiff unreasonably failed to make the modification permanent.

On October 20, 2009, one day after Wells Fargo had the Court’s order of a stay of discovery in which Defendant had asked for production of the original note, Wells Fargo unreasonably denied Defendant’s loan modification, Exhibit 2.

Second: Wells Fargo suggests it may “win” foreclosure on the mortgage but this is not the case. There have been two previous actions on the mortgage, each of which was voluntarily dismissed. The second dismissal constituted an adjudication upon the merits, pursuant to Rule 1-041(A)(1) and res judicata therefore bars this third action.

Background

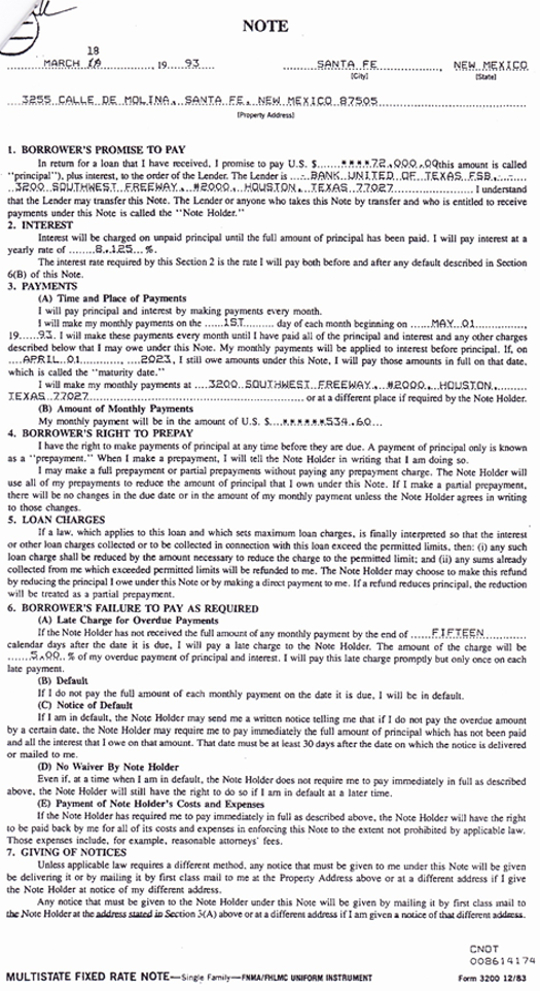

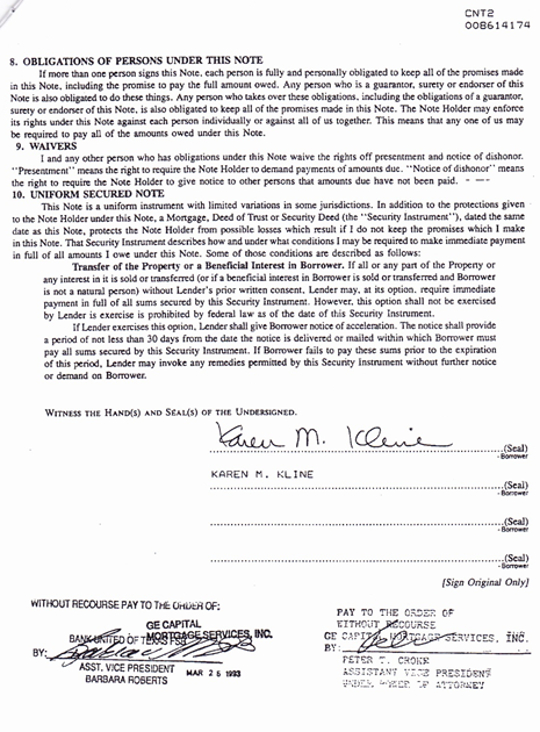

In March 1993, Kline executed a fixed rate note and mortgage in the amount of $72,000. The note was subsequently endorsed to G.E. Capital Mortgage Services, Inc., Exhibit 3, to which the successor by merger was G.E. Capital Mortgage Services, LLC, which assigned the mortgage to Wells Fargo Bank, N.A. on July 1, 2005, see Exhibit 1 to Motion to Dismiss for Failure to State a Claim Upon Which Relief Can Be Granted, (“Motion to Dismiss”).

On March 21, 1996, G.E. Capital Mortgage Services, Inc., filed a complaint for foreclosure, see Motion to Dismiss, Exhibit 2, with a copy of the note and mortgage attached, see Motion to Dismiss, Exhibit 3. On August 23, 2000, G.E. Capital Services, Inc. filed a Stipulation of Dismissal, voluntarily dismissing the complaint pursuant to SCRA 1-041, see Motion to Dismiss, Exhibit 4.

On February 27, 2004, G.E. Capital Mortgages Services, LLC., filed a complaint for foreclosure with the same note and mortgage attached. On January 9, 2006 plaintiff filed a motion to dismiss the complaint and on January 17, 2006, the complaint for foreclosure was dismissed, see Motion to Dismiss, Exhibit 5.

Certainly, the trail judge considered the motion a voluntary dismissal under Rule 1-041, as he dismissed all of the claims without prejudice and did not require compliance with customary motion procedure in doing so. (Labeling a filing as a “notice” or a “motion” in not controlling as to this issue. See United States v. 1982 Sanger 24’ Spectra Boat, 738 F.2d 1043, 1046 (9th Cir. 1983) (holding a “moving party’s label for its motion is not controlling”); Williams v. Ezell, 531 F.2d 1261, 1263 (5th Cir. 1976) (commenting “that it [the motion] was styled a ‘Motion for Dismissal’ rather than a ‘Notice of Dismissal’ is, in our opinion, a distinction without a difference”); Roddy v. Dendy, 141 F.R.D. 261, 261 (S.D. Miss. 1992) (holding denomination of a motion rather than a notice is “without legal significance since the effect desired . . . was clearly to have [plaintiff’s] claims dismissed without prejudice”).

The Seventh Circuit now follows the majority rule, see Smith v. Potter, 513 F.3d 781, 783 (7th Cir. 2008) (construing “motion to voluntarily dismiss the plaintiff’s complaint” as a Rule 41(a)(1) motion despite the plaintiff’s counsel having mis-captioned the filing).) In Janssen v. Harris, Jansen, 321 F.3d998 (10th Cir. 2003) at 1000-01, the Tenth Circuit construed a pro se plaintiff’s letter requesting dismissal of his case without prejudice as a Notice under Rule 41(a)(1), despite the fact that the letter did not mention Rule 41. In so doing, the Tenth Circuit emphasized the absolute right of a plaintiff to dismiss without prejudice. In Janssen, as in the present case, the plaintiff invited action by the courtby requesting dismissal, but the request was nonetheless construed as a Rule 41(a)(1) notice.))

In both the 1996 and the 2004 foreclosure actions the plaintiff alleged a default under the same note and mortgage, invoked the acceleration clause declaring the entire debt due, and prayed for judgment in foreclosure of the note, plus interest.

On April 7, 2008, Wells Fargo, as assignee, filed complaint for foreclosure in the present action attaching the same note and mortgage, declaring the entire debt due and asking for interest. (Two-dismissal rule, and thus doctrine of res judicata, applied to mortgagee’s assignee in foreclosure action even though two prior foreclosure actions, which resulted in voluntarily dismissals, were brought by mortgagee, not assignee; assignee was in privity with mortgagee and stood in mortgagee’s shoes. EMC Mtge. Corp. v. Jenkins, 841 N.E.2d 855 (Ohio App. 10 Dist. 2005).

Nothing in rule governing voluntary dismissals limits the preclusive effect of a second voluntary dismissal solely to the plaintiff who has twice dismissed; rather, the rule simply deems the claim twice dismissed adjudicated on the merits, and if the adjudicated claim is again refiled, principles of res judicata take over to determine whether the adjudication on the merits bars the refiled claim. Ibid.

Doctrine of res judicata is not limited to cases where the parties to the later action are identical to those in the earlier action; rather, res judicata also applies where there is privity between the parties in the two cases. Ibid. An assignee stands in the shoes of the assignor and succeeds to all the rights and remedies of the latter. Ibid. An assignee of an interest in a promissory note and mortgage is in privity with its assignor for purposes of res judicata. Ibid.)

In the June 10, 2011 deposition of Defendant Kline, Wells Fargo confirmed that the mortgage it seeks to foreclose is the same one Defendant signed in 1993, and Wells Fargo confirmed that the loan modification was concluded in March, 2000. March, 2000 is before the August, 2000 voluntary dismissal of the first foreclosure action by the Plaintiff. See Plaintiff’s Supplemental Brief on the State of the Law on Lost Notes, pages 5 to 9.

Two-dismissal rule – Adjudication of the Merits –

Res judicata – Foreclosure actions

In the instant case, the underlying note and mortgage are the same in the first two foreclosure actions as in the third. The key is that the whole note became due based on the acceleration clause. An Acceleration clause, as defined by Black’s Law Dictionary (7th Ed. Rev. 1999), requires the maker, drawer or other obligor to pay part or all of the balance sooner than the date or dates specified for payment upon the occurrence of some event or circumstance described in the contract, such as a default by nonpayment.

In a contract with an acceleration clause, a breach constitutes a breach of the entire contract. Once G.E. Capital invoked the note’s acceleration clause, the contract became indivisible with one obligation: to pay the entire balance on the note. Successive actions on the same note and mortgage do not involve different claims and there is nothing in Rule 1-041(A) that indicates it should not apply to foreclosure cases.

In order for res judicata to bar a subsequent action, the claims asserted therein need not be identical to the claims asserted in the prior action; rather, a valid, final judgment rendered upon the merits bars all subsequent actions based upon any claim arising out of the transaction or occurrence that was the subject matter of the previous action.

WHEREFORE Defendant respectfully asks the Court to dismiss this foreclosure action for failure to state a claim upon which relief can be granted.

Respectfully submitted,

Karen Marie Kline

Santa Fe, New Mexico 87507

— email: karenkline@q.com

CERTIFICATE OF SERVICE: I caused a true copy of DEFENDANT KAREN MARIE KLINE’S BRIEF ON LOST ORIGINAL NOTE to be mailed today, September 5, 2011, to: Castle, Stawiarski, Nathan E. Winger, 20 First Plaza NW Suite 602, Albuquerque, NM 87102

Exhibit 1

Exhibit 2

Exhibit 3

Exhibit 3

(303) 285-2222

Free Trials

Try Amazon Music Unlimited 30-Day Free Trial