HAMP loan modifications could have been heroic. But, no.

President Obama’s Secretary of the Treasury, Tim Geithner

10/14/2017 ~ Judge Ortiz has decided for Wells Fargo, and foreclosed my home. My lawyer let me down pretty dismally when he filed my Answer to Wells Fargo’s Amended Complaint late. I had begun fighting the Court’s decision to allow Wells Fargo to amend when they hadn’t actually shown they had the Original Note at the time it was lost, but my lawyer said no, the best thing to do was Answer and go forward. Then he filed my answer late, Wells Fargo asked for it to be struck, and Judge Ortiz struck my affirmative defenses and counterclaim. Not ideal.

Fraudulent Denial of Modification

The 7th Circuit’s March, 2012 opinion in Wigod v. Wells Fargo supports everyone who was offered a HAMP trial period and then was dishonestly and/or fraudulently denied loan Modification after successfully completing the trial period.

The HAMP guidelines are clear. Wells Fargo, however, has not followed those guidelines with me. I therefore looked for the place to complain and found the Comptroller of the Currency Administrator of National Banks. I learned that I was required to try to solve my problems with Wells Fargo before complaining. Thus, I wrote the letters below.

Office of the Comptroller of the Currency, Department of the Treasury ~ Read more.

HAMP wasn’t meant for us

7/12/2017 ~ It appears that HAMP was not really mean for us, you and me. In Bailout: An Inside Account of How Washington Abandoned Main Street While Rescuing Wall Street, Barofsky writes,

If the modifications were made permanent, Treasury required the servicer to waive the fees, but if the servicer canceled the modifications (say, for example, for the borrowers’ alleged failure to provide the necessary documents), the services could typically collect all of the accrued late fees once the homes were sold through foreclosure… One particularly pernicious type of abuse was that servicers would direct borrowers who were current on their mortgages to start skipping payments, telling them that that would allow them to qualify for a HAMP modification. The servicers thereby racked up more late fees, and meanwhile many of these borrowers might have been entitled to participate in HAMP even if they had never missed a payment.

A class action lawsuit filed against Bank of America revealed that low-level employees who lied to borrowers and the Treasury Department about the status of HAMP applications were rewarded with Target gift cards.

Bank of America would simply throw out documents on a consistent basis.

President Obama’s Secretary of the Treasury, Tim Geithner

When grilled, Treasury Secretary Geithner blurted out, ‘We estimate that they can handle ten million foreclosures, over time,’ referring to the banks. ‘This program will help foam the runway for them.’

A lightbulb went on for me. Elizabeth had been challenging Geithner on how the program was going to help home owners, and he had responded by citing how it would help the banks.

If you are in foreclosure you would do well to look carefully at the Complaint to see if there is evidence attached to demonstrate that the lender has standing to foreclose. Standing is essential. When a plaintiff does not have standing the case can and should be dismissed.

There may be a copy of a mortgage and note attached to the Complaint for Foreclosure, but it’s very possible they are not relevant and do not show that the would-be plaintiff has standing. Take a moment and read my Motion to Dismiss for Lack of Standing.

My Motion to Dismiss for Lack of Standing is based on a recent New Mexico Supreme Court case, which is published, Bank of New York v. Romero. I had to read it a few times to “get” it, especially since Wells Fargo’s lawyer quoted it sometime ago as if it supported the bank. The lawyer is very nice, the way a fisherman’s lure is nice from the viewpoint of fish.

Be sure you do Discovery if you are in foreclosure. Request the Original Note. The UCC requires that the plaintiff in a foreclosure produce the original note. Read more.

Also, but more tricky:

Res judicata can stop foreclosure

If you have had your home in two foreclosure actions on the same mortgage and both were dismissed, following which another foreclosure is filed, the third foreclosure is barred just as if the claims had been fully adjudicated on their merits. This is because once there is a final judgment in a court action, no further case can be filed for that cause of action.

Going to Court Pro Se and Causes of Action ~ Read more.

Sometimes a single previous foreclosure on the same mortgage can prevent a second foreclosure action.

Stopping Foreclosure using Res Judicata ~ Read more.

June 8, 2010 – I filed my OCC complaint today after I received a dishonest letter written by Wells Fargo Home Mortgage, apparently, to reply to my letter to Wells Fargo’s President and CEO, John G. Stumpf. (All three things are posted chronologically further down this page.)

May 3, 2010 – Wells Fargo is not considered a national bank for the purpose of complaining to the Comptroller of Currency about violations of the HAMP guidelines. GAO (Government Accounting Office) appears to say complaints to company presidents worked best. Since I objected OCC has clarified their site to include Wells Fargo as a national bank.

It’s stressful knowing Eric Holder, DOJ, was previously a Wells Fargo lawyer ~Your Nerves vs. Foreclosure ~ Read more.

Letters to and from Wells Fargo re: Home Affordable Modification Program (HAMP)

Karen Marie Kline

Santa Fe, New Mexico 87507

Loan number XXXXXXXX

Number at top of letter from you: XXXXXXXX

October 28 , 2009

Written Correspondence

Wells Fargo Home Mortgage

PO Box 10335

Des Moines, IA 50306-0335

Dear Wells Fargo,

Before I write for help from US government entities assigned to deal with bank/mortgage problems, I have been advised to write to you in hopes of resolution. I am, therefore, writing to you.

My problem is that Wells Fargo and its lawyers appear to be using HAMP loan modification to avoid discovery rather than for the purpose for which it was created and I am asking Wells Fargo: 1.) to recognize that I finalized Wells Fargo’s offer of a trial period in HAMP when I called Wells Fargo on September 26, 2009 and scheduled my three HAMP trial period payments; 2.) to send me the package of information that I was promised by Wells Fargo in the event I finalized Wells Fargo’s offer of a HAMP trial period; and 3.) to remove any legal fees that were or might be billed to me from September 22, 2009 when I was offered the HAMP trial period, or alternatively from September 26, 2009 when I finalized my acceptance of the offer.

Here is what has happened:

I applied to Wells Fargo for Home Affordable Modification Program help in March, 2009. I enlisted HOPE NOW help and a counselor called in with me several times. During one call, several months down the road, we were told that my file had not been updated since 2005.

I repeatedly complied with Wells Fargo’s requests that I send in my documents with current dates and new signatures.

At the same time I have been counterclaiming in Wells Fargo’s foreclosure action that Wells Fargo has dealt with me in bad faith. In order to prosecute my case Isent Interrogatories and Requests for Production to Wells Fargo via its lawyers. In response I was given only three answers: the name of the person actually answering the questions, her job title: lawyer, and her work address.

Thereafter I sent a letter pursuant to rule 1-037 NMRA requesting proper answers to my other questions and I explained why I needed them. When the deadline for proper responses drew near Ms. Charney’s legal assistant called me and said that they weren’t going to answer my discovery and that I was in a forbearance plan. Only I’d never heard about any forbearance plan prior to the legal assistant mentioning it.

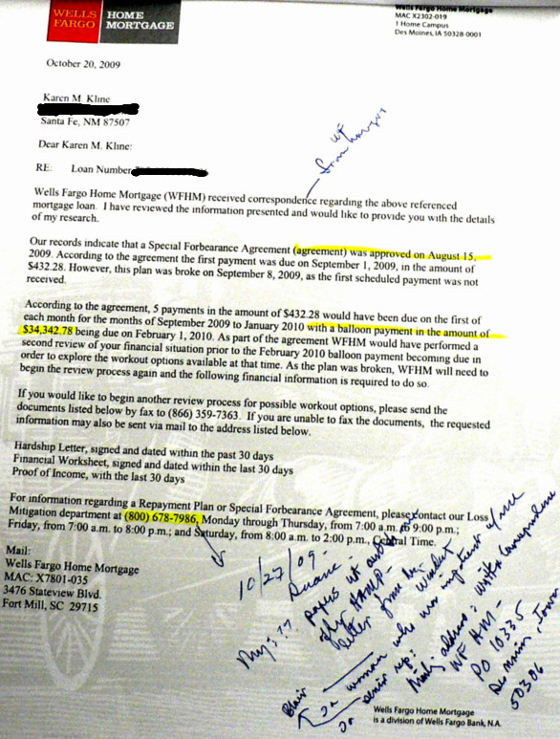

Thereafter Wells Fargo sent me a letter saying there was a moratorium during the forbearance plan, and that I should sign the enclosed agreement. However, the agreement said I would pay $480+/- a month on my mortgage followed by a balloon payment in February, 2010 of about $34k. I don’t have that kind of money, for either the $480 monthly payments or the huge balloon, so I could not in honesty sign the agreement and I did not.

I filed with the court a statement that I would agree to a two week delay but after that I had to work on prosecuting my case. Although Ms. Charney and her assistant said they would file something re the moratorium, they did not file anything.

In time I sent Wells Fargo Requests for Admissions, many of which mirrored my Interrogatories. None of my Admissions was timely denied. As a result the Admissions are deemed admitted and conclusively established under Rule 1-036 NMRA.

Meanwhile, on September 22, 2009, just before the deadline to deny, Wells Fargo wrote to me offering a Home Affordable Modification Program Trial Period. In its letter Wells Fargo wrote that I could “finalize this offer” by calling in by October 6, 2009 so that Wells Fargo could “establish your trial modification plan.” The letter also said, “Within a week of setting up your trial period, we will send you a package of information that clearly spells out the full terms and the documentation you need to supply.”

I finalized the offer by calling in on September 26, 2009 and scheduling three modification plan payments for which I was charged $20 (whereas Wells Fargo’s letter had said it would be free). Thereafter I did not receive the package of information that had been promised in the September 22, 2009 letter.

At the same time Wells Fargo’s lawyers refused to agree to vacate the October 19, 2009 foreclosure hearing on Wells Fargo’s motion for summary judgment. This was particularly worrying to me because HAMP guidelines specifically say that foreclosure is to be suspended during the trial period.

At the last minute Wells Fargo’s lawyers produced a motion to continue, while still refusing to sign the simple order I had proposed to vacate the hearing. I objected that continuing is not the same as suspending. Ms. Charney refused to talk to me on the phone about the October 19, 2009 summary judgment hearing. She hung up when I answered and did not return any of my three calls when I called back and left messages. I also objected that the lawyers were dishonest in their motion to continue and had falsified the order when they filled in the line above my name saying they had been unable to reach me.

At the hearing I quoted from the Home Affordable Modification Program Guidelines repeatedly and repeatedly said that the hearing should not have been held.

On October 27, 2009, I received a letter from Wells Fargo dated October 20, 2009 saying that a forbearance plan had been approved (failing to note that I had not been able to agree because of the huge amounts of money it required from me) and that because I did not keep the agreement I was taken out of the trial period.

I immediately called Wells Fargo at the number listed: 1-800-678-7986, and spoke with a series of Wells Fargo representatives beginning with Duane, and progressing to a senior rep named Blair. Basically I was told that on October 20, 2009 Wells Fargo’s lawyers told Wells Fargo to take me out of the HAMP trial period.

I am concerned by this because it appears to be a tactic meant to punish me for not going along with the deceit the lawyers incorporated into their Motion to Continue, as well as a tactic to avoid responsibility for refusing to vacate the hearing on their motion for summary judgment which the HAMP guidelines clearly say should not have been held while I was in the trial period.

The problem, then, is that Wells Fargo and its lawyers appear to be using the HAMP trial period to avoid discovery rather than for the objectives identified by the United States government when the program was set up and Wells Fargo agreed to participate; and, Wells Fargo’s lawyers appear to have violated the HAMP guidelines be refusing to sign the simple order vacating Wells Fargo’s summary judgment hearing.

Further, it is not acceptable under HAMP to ask me, a borrower, for cash for the Modification, so that appears to mean that the $20 fee to set up my three trial period payments was not envisioned by the US Treasury.

Arbitrarily excusing/explaining the termination of my HAMP trial period on the basis of my non-agreement to the $34k balloon payment that was part of Wells Fargo’s $480+/- monthly payment forbearance plan appears to violate the same HAMP guideline. (I’m not sure it was all right for Wells Fargo to ask me to pay the Escrow Account, which I did pay in the amount of more than $400.)

The fact that Wells Fargo said it would not cooperate with discovery, the fact that my HAMP trial period was instituted before a critical discovery deadline, and the fact that Wells Fargo and its lawyers arbitrarily terminated my trial period the day after the prohibited hearing at which they were given a stay of discovery, gives the appearance of Wells Fargo using the HAMP program to avoid discovery.

In order to resolve the foregoing problems in the simplest terms possible I am asking Wells Fargo: 1.) to recognize that I finalized Wells Fargo’s offer of a trial period in HAMP when I called Wells Fargo on September 26, 2009 and scheduled my three HAMP trial period payments; 2.) to send me the package of information that I was promised by Wells Fargo in the event I finalized Wells Fargo’s offer of a HAMP trial period; and 3.) to remove any legal fees that were or might be billed to me from September 22, 2009 when I was offered the HAMP trial period, or alternatively from September 26, 2009 when I finalized my acceptance of the offer.

Sincerely,

Karen Marie Kline

Wells Fargo responded unbelievably quickly

Santa Fe, New Mexico 87507

Loan number XXXX

Number at top of letter from you: XXXXX

November 8, 2009

Monika Leuang Van

Written Correspondence

Wells Fargo Home Mortgage

PO Box 10335

Des Moines, IA 50306-0335

Dear Ms. Van,

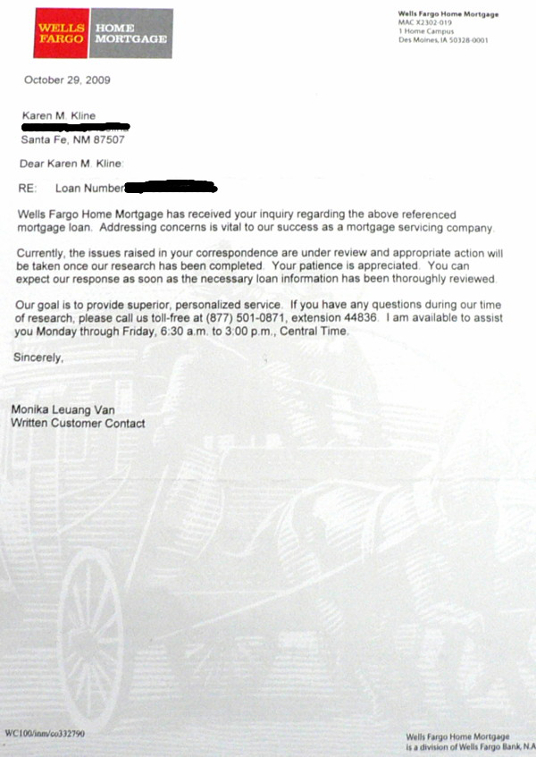

Your letter dated October 29, 2009 sounds generic and doesn’t answer any of my questions.

Basically, I am concerned that Wells Fargo Home Mortgage used the Home Affordable Modification Program (“HAMP”) trial period to avoid discovery rather than for its intended purpose. I was about to write to the Comptroller of the Currency Administrator of National Banks to complain when I read that I’m supposed to write to the bank first, that’s why I wrote to Wells Fargo Home Mortgage Written Correspondence.

Here, more concisely are my questions:

1. Why I was not sent the things which Sr. Vice President Ben Windust’s letter of September 22, 2009 clearly stated would be sent to me after I finalized my acceptance of Wells Fargo’s HAMP trial period offer by calling in before October 6, 2009 and scheduling three payments at the new rate provided to me under HAMP? (I finalized on September 26, 2009.)

2. When will I be sent the things that were promised if I finalized Wells Fargo’s HAMP trial period offer?

3. Where in HAMP US Treasury Guidelines does it permit lawyers to use the trial period to avoid discovery? (Wells Fargo phone reps said the correspondence upon which my cancellation was based was from Wells Fargo lawyers.)

Surely my “necessary loan information” was thoroughly reviewed before offering me the HAMP trial period. Wasn’t it? So, the questions now are those above: 1-3.

I look forward to your specific answers and to having my finalized trial period reinstated. I will gladly wait another ten days for resolution.

Sincerely,

Karen Marie Kline

Santa Fe, New Mexico 87507

Loan number XXXXX

Number at top of letter from you: XXXXX

November 8, 2009

Ben Windust, Senior Vice President

Wells Fargo Home Mortgage

PO Box 10368

Des Moines, IA 50306-0368

Dear Mr. Windust,

When I called Wells Fargo Home Mortgage about the cancellation of my Home Affordable Modification Program (“HAMP”) trial period after I had finalized my acceptance of Wells Fargo’s offer, see attached letter from you with my notes, and one day after Wells Fargo achieved a stay of my discovery I was told to write to “Written Correspondence”; a copy of my letter is attached.

Wells Fargo’s response dated October 29, 2009 sounds generic and doesn’t answer any of my questions.

Basically, I am concerned that Wells Fargo Home Mortgage used the HAMP trial period offer that it extended to me to avoid discovery rather than for the trial period’s intended purpose. I was about to write to the Comptroller of the Currency Administrator of National Banks to complain when I read that I’m supposed to write to the bank for resolution first.

Here are my questions and the issues needing resolution:

1. Why I was not sent the things which your letter of September 22, 2009 clearly stated would be sent to me after I finalized my acceptance of Wells Fargo’s HAMP trial period offer by calling in before October 6, 2009 and scheduling three payments at the new rate provided to me under HAMP? (I finalized on Saturday, September 26, 2009.)

2. When will I be sent the things that were promised to me by you and Wells Fargo if I finalized Wells Fargo’s HAMP trial period offer?

3. Where in HAMP US Treasury Guidelines does it permit lawyers to use the trial period to avoid discovery? (Wells Fargo phone reps said the correspondence upon which my cancellation was based was from Wells Fargo lawyers. See attached letter.)

I look forward to specific answers and to having my finalized trial period reinstated.

Because I began asking Wells Fargo Home Mortgage for Home Affordable Modification in March, 2009, and, I resubmitted my information on a nearly monthly basis, I trust Wells Fargo Home Mortgage had ample time to thoroughly review my necessary loan information prior to you sending me Wells Fargo’s offer of the HAMP trial period.

That being true, I trust that ten additional days will be ample time for resolution of the issues that I have presented to include reinstating my HAMP trial period and sending me the promised materials and documents.

Sincerely,

Karen Marie Kline

Copy of 1st letter on this page also attached…

Wells Fargo’s Less than Honest Response

Karen Marie Kline XXXXX Santa Fe, New Mexico 87507 Loan number XXXXXXXX

February 8, 2010

Ben Windust, Senior Vice President, and Sarah Butts Wells Fargo Home Mortgage PO Box 10368 Des Moines, IA 50306-0368

Dear Mr. Windust and Sarah Butts,

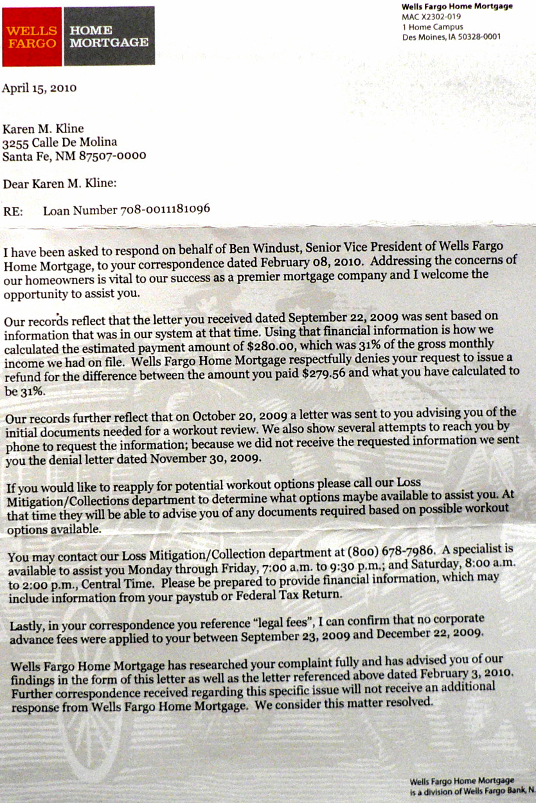

Your letter dated February 3, 2010 cannot be true given what your previous letters actually said.

For instance, your September 22, 2009 letter, attached, said that after I finalized my “acceptance of this offer” by calling in before October 6, 2009 and scheduling three payments at the new rate Wells Fargo would send me “a package of information that clearly spells out the full terms and the documentation you need to supply.” I finalized on Saturday, September 26, 2009 but Wells Fargo never sent me the promised package of information.

Your September 22 letter also said, “During this phone call, we’ll schedule a date for your first trial payment.” That was done, the trial payment was scheduled, as were the subsequent two payments which your letter of September 22 talked about: “You will need to make two additional payments,” and that too was done. Wells Fargo accepted and cashed over a three month period my three trial period payments, yet no information was sent to me.

Then, when I was denied just before the end of three months, the letter said I had been denied because I had not sent in all the things I had been asked for, only as stated above, no package stating what I needed to send in was ever sent to me: I was not asked for anything.

In terms of Wells Fargo taking my social security supplemental income, that was a part of my GROSS income.

The amount that was demanded in the HAMP letter from Mr. Windust and subsequently taken by Wells Fargo was supposed to have been 31%. Only Wells Fargo took more than 31% of my gross income.

Whether I was accepted or denied, the fact is that Wells Fargo offered me a HAMP trial period, I did what I was asked, even though the amount, demanded (as I later learned) was not acceptable under the government terms of the program. I was denied only after Wells Fargo took all of my supplemental income on top of the allowable 31%. My supplemental income which was taken in excess of what the HAMP program designates must be returned to me.

I am reiterating: In order to resolve the problems in the simplest terms possible I am asking Wells Fargo: 1.) to recognize that I finalized Wells Fargo’s offer of a trial period in HAMP when I called Wells Fargo on September 26, 2009 and scheduled my three HAMP trial period payments as outlined in Mr. Windust’s September 22, 2009 letter; 2.) to send me the package of information that I was promised by Wells Fargo in the event I finalized Wells Fargo’s offer of a HAMP trial period; 3.) to remove any legal fees that were or might be billed to me from September 22, 2009 when I was offered the HAMP trial period, or alternatively from September 26, 2009 when I finalized my acceptance of the offer; and 4.) to return to me my supplemental income which was taken in excess of 31% of my gross income.

Sincerely,

Karen Marie Kline

Again Wells Fargo sent a questionable response

Karen Marie Kline XXXXXXXXXXX Loan number XXXXXXXXXXX April 30, 2010 Ben Windust, Senior Vice President, and Sarah Butts Wells Fargo Home Mortgage PO Box 10368 Des Moines, IA 50306-0368

Dear Mr. Windust and Sarah Butts,

Key statements in your April 15, 2010 letter, mailed April 19, 2010 are either mistakes or malicious dishonesty. Plus, your letter shows a clear violation by Wells Fargo of Home Affordable Modification Program (HAMP) guidelines. Therefore I must ask you some questions (basic to my complaint to the OCC Administrator of National Banks/Treasury):

1. How did the Wells Fargo system have incorrect financial information for me “at that time” (September 22, 2009) when I had sent in my correct financial information, to include banks statements and budget verified by Hope Now representatives, on May 21, 2009:

Time: 5/21/2009 2:31:19 PM Sent to 8663597363 with remote ID “” Result: (0/339;0/0) Successful Send Page record: 1 – 17 Elapsed time: 13:56 on channel 13

2. Without change from May 21, 2009 to September 22, 2009 my income consisted of social security, supplemental income, and a few dollars a month from my website, together adding up to $704; so why did Wells Fargo say 31% of my income was $279.56? Isn’t 31% of $704 actually $218.24?

3. Isn’t it true that $218.24 plus my $62 supplemental income, which I get because of my disability, adds up to $280.24 which is less than a dollar different from the $279.56 Wells Fargo falsely said was 31% of my income?

4. If 31% of my income was actually $218.24, but Wells Fargo wrongly calculated it to be $279.56, then isn’t it true that Wells Fargo owes me a refund of $61.32, which is the difference, for each of three months?

5.And, isn’t it true that $61.32 is almost exactly the amount of my supplemental income which is $62.00?

6. Isn’t it true that the Home Affordable Modification Program (HAMP) says, “Servicers will follow the Standard Waterfall described below to reduce monthly payments to the 31% Front-End DTI Target defined above” ?

7. Isn’t it true that the Home Affordable Modification Program says, “The investor may not require the borrower to contribute cash” ?

8. It is also true, isn’t it, that Wells Fargo in its October 20, 2009 letter, copy attached, which you referenced, asked me to contribute $34,342.78?

9. Because the lender is disallowed by HAMP from requiring me to contribute cash, the October 20, 2009 letter requiring $34,342.78 could not be the package of requirements for HAMP that was promised to me in the September 22, 2009 letter. Isn’t that true? Or, is it a violation of HAMP guidelines?

10. Why were no messages left for me if indeed attempts were made to reach me by phone after September 22, 2009?

11. Why, prior to September 22, 2009 and prior to the offer of HAMP loan modification, did Wells Fargo employees hang up when I answered the phone? (See my letter of October 28, 2009.)

I am reiterating: In order to resolve the problems in the simplest terms possible I am asking Wells Fargo: 1.) to recognize that I finalized Wells Fargo’s offer of a trial period in HAMP when I called Wells Fargo on September 26, 2009 and scheduled my three HAMP trial period payments as outlined in Mr. Windust’s September 22, 2009 letter; 2.) to send me the package of information that I was promised by Wells Fargo in the event I finalized Wells Fargo’s offer of a HAMP trial period; 3.) to remove any legal fees that were or might be billed to me from September 22, 2009 when I was offered the HAMP trial period; 4.) to return to me $61.32 times three for the three monthly payments I made, since the $61.32 was required in excess of 31% of my gross income: and 5.) to provide a proper 31% HAMP payment with the package of information.

I will not be calling you directly, but thank you for your number. I have a brain injury and it’s hard for me to talk. It’s much easier to write, since that is slower.

Sincerely, Karen Marie Kline

Karen Marie Kline XXXXXXXXXXXX Santa Fe, New Mexico 87507 May 13, 2010 John G Stumpf, President and CEO Corporate Offices Wells Fargo 420 Montgomery Street San Francisco, CA 94104

Dear Mr. Stumpf,

I am one of your mortgage loan customers and I am writing to you because I am frustrated and concerned by the way my mortgage loan has been handled in relation to the Home Affordable Modification Program (HAMP).

I was offered a HAMP trial modification period, which I finalized by timely calling in and scheduling payments as per the 9/22/09 letter I was sent by Ben Windust.

What happened thereafter makes it appear that Wells Fargo Home Mortgage’s offer of a HAMP trial modification period was in bad faith and fraudulent.

I have tried to address these problems by writing to Ben Windust.

The responses I received, however, signed by Sarah Butts, raise questions rather than resolve problems.

I hope you will help me.

Here is a summation I am preparing in order to complain to the Office of the Comptroller of Currency:

To resolve my complaint that Wells Fargo acted in bad faith, with deceit and fraud, in handling my mortgage in a HAMP trial period I asked WF to recognize that I finalized WF’s 9/22/09 HAMP trial period offer when I called WF on 9/26/09 and scheduled three payments; to send me the package of information I was promised; to remove legal fees since 9/22/09; to return $61.32 (required in excess of 31% of my gross income) times three; and to provide a proper 31% HAMP payment with the information package.

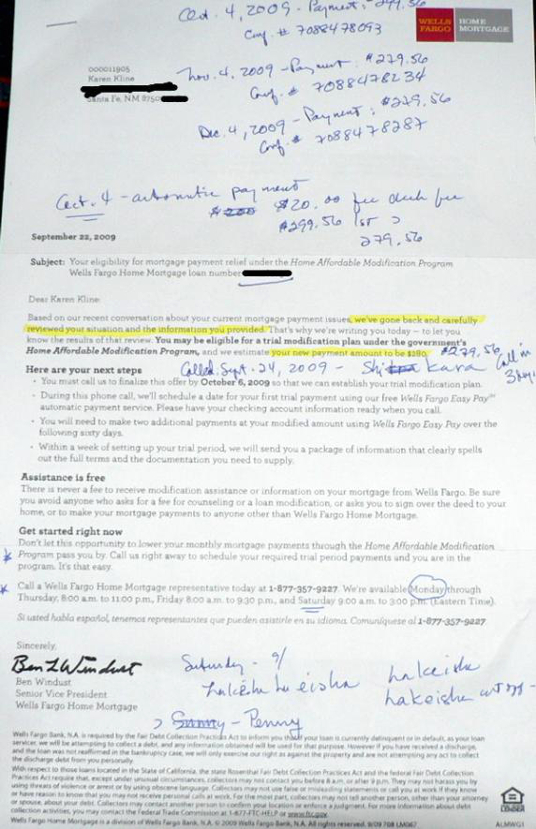

Chronology: On 9/22/09, Ben Windust, Sr. V.P., WF Home Mortgage, wrote, “We’ve gone back and carefully reviewed your situation and the information you provided… You may be eligible for a trial modification plan under the government’s Home Affordable Modification Program… You must call us to finalize this offer by October 6, 2009 so that we can establish your trial modification plan… During this phone call we’ll schedule a date for your first trial payment… You will need to make two additional payments… Within a week of setting up your trial period we will send you a package of information that clearly spells out the full terms and the documentation that you need to supply.”

I called on 9/24/09 and finalized. Three payments at the new rate of $279.56 were scheduled with a $20 check fee added to my 1st payment 10/4/09: $299.56 confirmation #7088478093; 11/4/09: $279.56 confirmation #7088478234; 12/4/09: $279.56 confirmation #7088478287.

The package of information promised in WF’s 9/22/09 letter was never sent.

Citing the HAMP trial period WF lawyers would not answer my discovery requests in my home’s foreclosure. At the same time WF lawyers would not vacate their 10/19/09 summary judgment hearing. At the hearing the judge stayed the case.

On 10/20/09, WF wrote that because I did not keep WF’s forbearance plan I was taken out of the trial period. WF’s 8/15/09 plan required a $34,342.78 balloon payment on 2/1/10. I did not have that nor could I afford $432.28 payments so I hadn’t signed.

On 10/27/09 I spoke with Duane at the number in WF’s 10/20/09 letter: 1-800-678-7986. He transferred me to a senior rep, Blair, who said that on 10/20/09 WF lawyers told WF to take me out of the HAMP trial period.

Still WF cashed my scheduled trial period payments, even after writing on 11/30/09, “after carefully reviewing the information you’ve provided, we are unable to adjust the terms of your mortgage. This decision was made because you did not provide us with all of the information needed within the time frame required per your trial modification…”

During the three months of trial period payments I did not have enough money to make ends meet so I wondered if $279.56 was 31% of my monthly income. It was not. 31% of my $704 income was supposed to be $218.24. So WF was taking $61.32 of my $62 supplemental income for my disability due to traumatic brain injury.

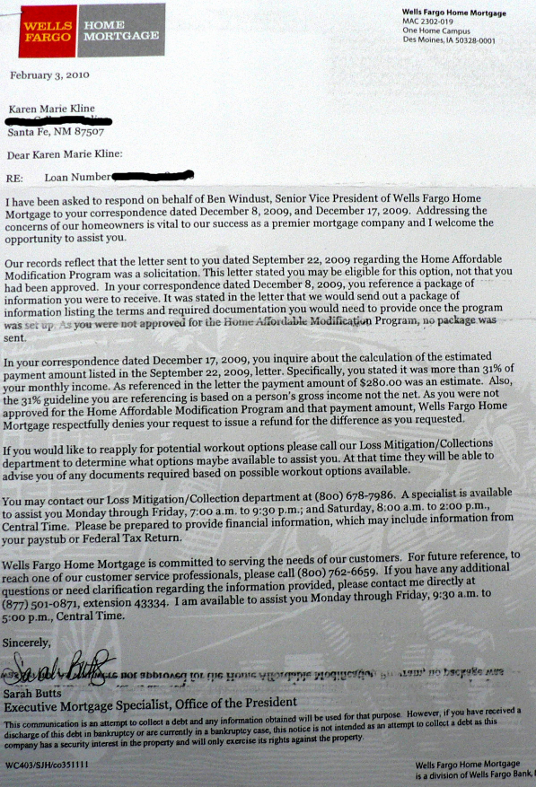

I wrote to Ben Windust about this, asking for a refund. Sarah Butts replied, 4/15/10, that WF used financial information they had on file for me “at that time,” so the payment was 31% and there would be no refund.

I wrote back that on 5/21/09 WF confirmed receipt of my correct, financial information: $704, verified by a HOPE NOW representative from Money Management International:

Time: 5/21/2009 2:31:19 PM Sent to 8663597363 with remote ID “” Result: (0/339;0/0) Successful Send Page record: 1 – 17 Elapsed time: 13:56 on channel 13

I wrote that my financial information had not changed.

Sarah Butts also wrote in her 4/15/10 letter that on October 20, 2009 I was sent the package of information I’d been promised.

I replied that lenders are disallowed by HAMP from requiring cash contributions so WF’s October 20, 2009 letter referencing a requirement of $34,342.78 could not be the package of requirements for HAMP that was promised in WF’s 9/22/09 letter.

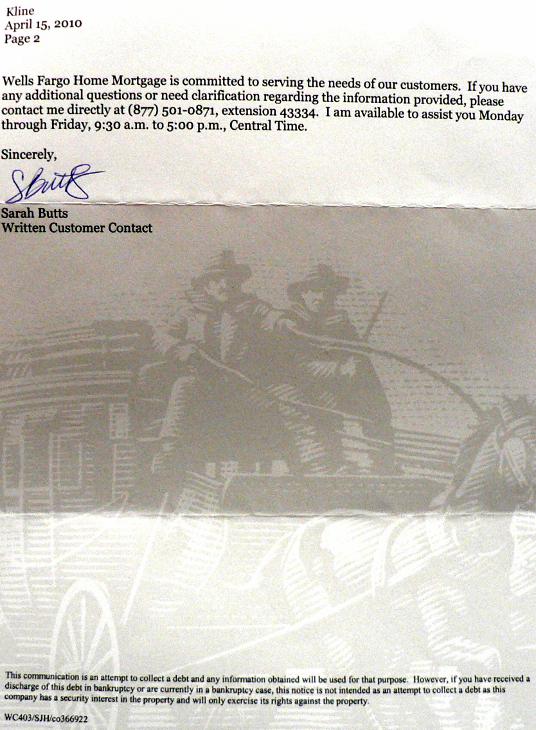

In her 4/15/10 letter, Sarah Butts concluded my case had been investigated, was now closed and she would not answer further letters.

I look forward to your help. I’ll hold off complaining to the Office of the Comptroller of Currency for ten working days in the hope of a response from you. I can’t wait longer because on Monday, May 10, 2010, I received a paper filed by Wells Fargo lawyers in the foreclosure.

Sincerely, Karen Marie Kline

Copies: Ben Windust, Senior Vice President Wells Fargo Home Mortgage PO Box 10368 Des Moines, IA 50306-0368

Sarah Butts Wells Fargo Home Mortgage PO Box 10368 Des Moines, IA 50306-0368

My 3,399 Character Complaint to the OCC

To resolve my complaint that Wells Fargo acted in bad faith with deceit and fraud in handling my mortgage’s HAMP trial period I asked WF to recognize that I finalized WF’s 9/22/09 HAMP trial period offer when I called WF on 9/26/09 and scheduled three payments; to send me the package of information I was promised; to remove legal fees since 9/22/09; to return $61.32 times three (required in excess of 31% of my gross income); and to provide a proper 31% HAMP payment with the information package. Copying to Wells Fargo’s president did not help.

Chronology: On 9/22/09, Ben Windust, Sr. V.P., WF Home Mortgage, wrote, “We’ve gone back and carefully reviewed your situation and the information you provided… You may be eligible for a trial modification plan under the government’s Home Affordable Modification Program… You must call us to finalize this offer by October 6, 2009 so that we can establish your trial modification plan… During this phone call we’ll schedule a date for your first trial payment… You will need to make two additional payments… Within a week of setting up your trial period we will send you a package of information that clearly spells out the full terms and the documentation that you need to supply.”

I called on 9/26/09 and finalized. Three payments at the new rate of $279.56 were scheduled with a $20 check fee added to my 1st payment: 10/4/09: $299.56 confirmation #7088478093; 11/4/09: $279.56 confirmation #7088478234; 12/4/09: $279.56 confirmation #7088478287.

The information package promised in WF’s 9/22/09 letter was never sent.

Citing the HAMP trial period WF lawyers would not answer my discovery requests in my home’s foreclosure. At the same time WF lawyers would not vacate their 10/19/09 summary judgment hearing. At the hearing the judge stayed the case.

On 10/20/09, WF wrote that because I did not keep WF’s forbearance plan I was taken out of the trial period. WF’s 8/15/09 plan required a $34,342.78 balloon payment on 2/1/10. I did not have that nor could I afford $432.28 payments so I hadn’t signed.

On 10/27/09 I spoke with Duane at the number in WF’s 10/20/09 letter: 1-800-678-7986. He transferred me to a senior rep, Blair, who said that on 10/20/09 WF lawyers told WF to take me out of the HAMP trial period.

WF cashed my scheduled trial period payments even after writing on 11/30/09, “after carefully reviewing the information you’ve provided, we are unable to adjust the terms of your mortgage. This decision was made because you did not provide us with all of the information needed within the time frame required per your trial modification…”

During the three months of trial period payments I did not have enough money to make ends meet. I wondered if $279.56 was 31% of my monthly income. It was not. 31% of my $704 income is $218.24. So WF was taking $61.32 of my $62 supplemental income for my disability due to traumatic brain injury.

I wrote to Ben Windust on 11/8/09 asking for a refund. Sarah Butts replied, 4/15/10, that WF used financial information they had on file for me “at that time,” so the payment was 31% and there would be no refund.

I replied that on 5/21/09 WF confirmed receipt of my correct, financial information: $704, verified by a HOPE NOW representative from Money Management International:

Time: 5/21/2009 2:31:19 PM Sent to 8663597363 with remote ID “” Result: (0/339;0/0) Successful Send Page record: 1 – 17 Elapsed time: 13:56 on channel 13

I wrote that my financial information had not changed.

Sarah Butts also wrote in her 4/15/10 letter that on October 20, 2009 I was sent the package of information I’d been promised.

I replied that lenders are disallowed by HAMP from requiring cash contributions so WF’s October 20, 2009 letter referencing a requirement of $34,342.78 could not be the package of requirements for HAMP that was promised in WF’s 9/22/09 letter.

Ms. Butts 4/15/10 letter said my case was investigated, closed, and no further letters would be answered.

I also wrote to Mr. Stumpf again

Karen Marie Kline XXXXXXXXXXX Santa Fe, New Mexico 87507 June 8, 2010 John G Stumpf, President and CEO Corporate Offices Wells Fargo 420 Montgomery Street San Francisco, CA 94104

Dear Mr. Stumpf,

I am one of your mortgage loan customers and I am writing to you because I am frustrated and concerned by the way my mortgage loan has been handled by Wells Fargo Home Mortgage in relation to the Home Affordable Modification Program (HAMP).

I wrote concerns of mine to you on May 13, 2010 and copied my letter to Wells Fargo Home Mortgage.

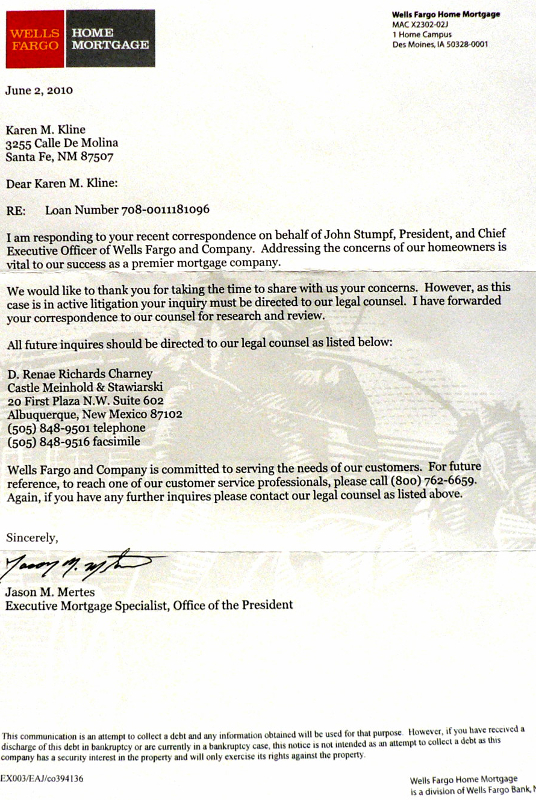

I have not had a response from you via your actual office. But, on June 2, 2010 Wells Fargo Home Mortgage’s Jason M. Mertes wrote a questionable letter to me saying that my loan is in active litigation. This is not true. The case was stayed because of the HAMP trial period and I have received nothing from the court indicating that the stay has been lifted.

Indeed the stay should not be lifted because I did everything required to finalize my HAMP trial period modification, and therefore my loan modification should be finalized by Wells Fargo Home Mortgage.

I will not be calling your legal counsel who, you should be aware, has in the past hung up when they heard me answer the phone while they were leaving a message; additionally they have in the past refused to call me back when I left messages.

Sincerely, Karen Marie Kline

Copies: Ben Windust, Senior Vice President Wells Fargo Home Mortgage PO Box 10368 Des Moines, IA 50306-0368

Jason M. Mertes, Exec. Mortgage Specialist Wells Fargo Home Mortgage MAC X2302-02J I Home Campus Des Moines, IA 50328-0001